There are many people in India working in unorganised sectors with no guarantee of any pension at old age. Though government had launched Swavalamban Yojana in 2011-2012, a very less people joined the scheme as it did not provide any certainty of amount payable at vesting age.

To provide financial security to such people at older age government has announced the Atal Pension Yojana (APY), which will provide a defined pension, depending on the contribution, and its period. The APY will be focussed on all citizens in the unorganised sector, who join the National Pension System (NPS) administered by the Pension Fund Regulatory and Development Authority (PFRDA). Under the APY, the subscribers would receive the fixed minimum pension of Rs. 1000 per month, Rs. 2000 per month, Rs. 3000 per month, Rs. 4000 per month, Rs. 5000 per month, at the age of 60 years, depending on their contributions, which itself would be based on the age of joining the APY.

Eligibility Conditions of Atal Pension Yojana

Minimum Age at entry: 18 years

Maximum age at entry: 40 yrs

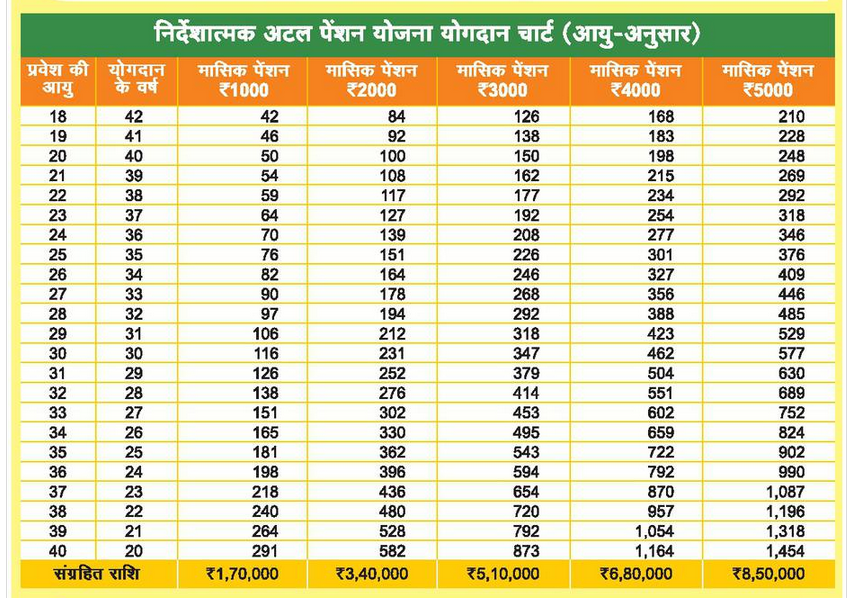

Period of contribution: 20 to 42 years (60- age at entry)

Pension amount payable at maturity age: Rs. 1000 to Rs. 5000 (depending upon age of entry and contribution)

Contribution per month: Rs. 42 to Rs. 1454 (depending upon at at entry and pension payable after age of 60)

Atal Pension Yojana (APY) is open to all bank account holders. The Central Government would also co-contribute 50% of the total contribution or Rs. 1000 per annum, whichever is lower, to each eligible subscriber account, for a period of 5 years, i.e., from Financial Year 2015-16 to 2019-20, who join the NPS before 31st December, 2015 and who are not members of any statutory social security scheme and who are not income tax payers. However, the scheme will continue after this date but Government Co-contribution will not be available.

Benefits of Atal Pension Yojana:

After the vesting age ie 60 years pension will be payable to as per the contribution done by the proposer ranging from Rs. 1000 to Rs. 5000 per month. In the event of death of the annuitant pension will be payable to spouse and there after purchase price (Fund on which pension is available ranging from Rs. 170000 to Rs. 850000) will be given to the nominee.

Contribution for Atal pension yojana:

Click to download Rules of Atal Pension Yojana

I am a income tax payer.My wife is housewife. can I do this pension scheme for my wife?

What is the procedure to close PMAPY and what about the amount, which has been deducted from last 3 months? I have an saving account in sbi…i visted saveral time to sbi bracnh including main sbi branch…they dont know about this scheme properly…please guide me..what to do ahead..

if i have take this plan of mothly pension plan rs 5000/- . and i have completed 60 years . after that i have received 5 time pension & than i had died than which amount is payble to nominee